Automotive Newsletter Q2 2022

Download PDF

Overview of M&A activity

Geopolitical tensions, record prices for oil and raw materials, as well as high inflation and increased interest rates weighed on the automotive sector in the second quarter of 2022. The semiconductor shortage in particular is expected to continue to impact global vehicle production through to 2024 and slow the transition towards electrification.

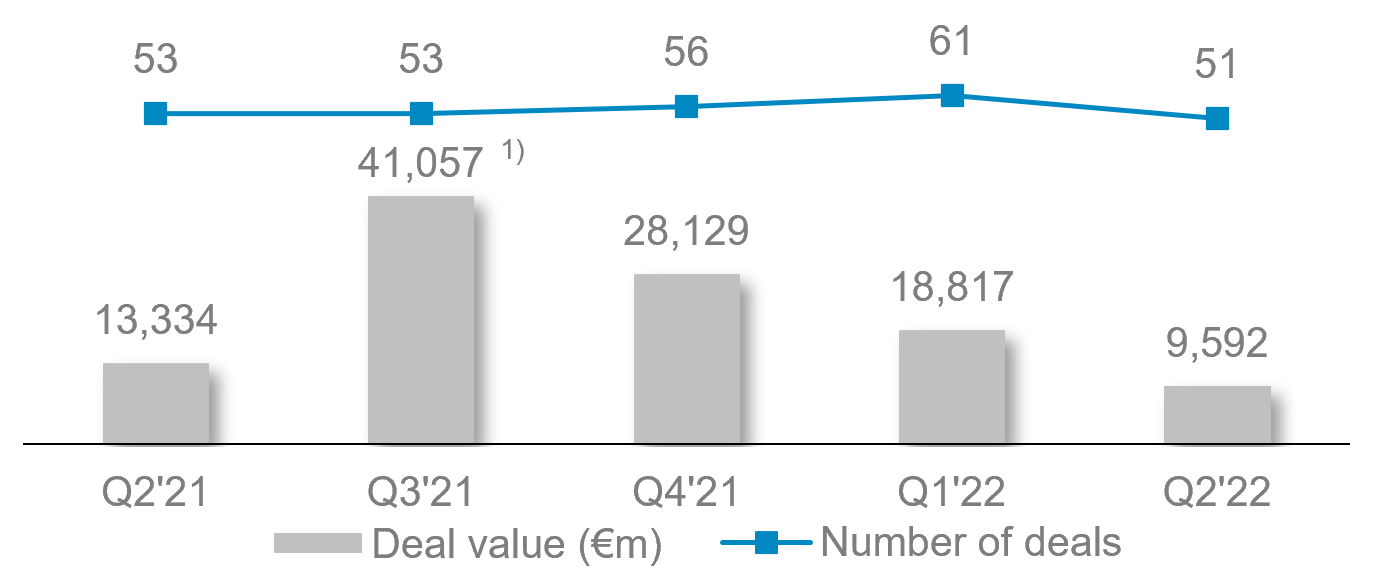

Activity decreased in Q2 2022 with a total of 51 completed transactions compared to 61 transactions in Q1 2022

These effects have also negatively impacted the global automotive M&A market. Activity decreased in Q2 2022 with a total of 51 completed transactions compared to 61 transactions in Q1 2022. In line with this development, the cumulative deal value has decreased in Q2 2022 (€9.6bn) compared to Q2 2021 (€13.3bn).

Contrary to this trend the areas of electromobility, connectivity and autonomous driving, as well as special situations M&A continue to show deal momentum with investments in companies such as Rimac, Inspiration Mobility and and the most recent capital increase and majority sale of Allgaier Group.

The valuation environment in Q1 2022 and Q2 2022 is still exposed to the uncertainties in the market. In Europe, EV/sales, EV/EBITDA and EV/EBIT multiples decreased by 3.8%, 1.5% and 2.9% respectively in Q2 2022. A similar trend can be observed in North America, albeit less pronounced, where EV/sales, EV/EBITDA and EV/EBIT multiples decreased by 3.2%, 1.5% and 1.8% respectively. Asia is the only region that has experienced an increase across all valuation multiples with EV/sales, EV/EBITDA and EV/EBIT multiples rising by 7.8%, 15.3% and 18.0% in Q2 2022, respectively.

Despite all uncertainties, pent-up demand for innovation will continue to drive the industry. Participants in the automotive industry can use this momentum to further push the transition to a net-zero world of transportation. Alongside the increasing improvements in electric vehicles, the opportunities in the advanced intelligent vehicle market will also drive the automotive industry with new driver assistance systems or network technologies to take vehicle safety to a new level.

M&A Activity: Quarterly Comparison Q2 2021 – Q2 2022

Top M&A Deals Q2 2022

- Allgaier Group, the Germany-based worldwide leading manufacturer of cold-formed, lightweight structural and car body systems, was acquired by Westron Group, a Shanghai-based industry group investing in companies that provide advanced solutions in the automotive and technology sector. The mutual aim of Westron and Allgaier is to strengthen and expand the automotive division, including the tool-making operations, and the process technology division, along with their various subsidiaries and locations.

- Rimac Group doo, the Croatia-based manufacturer of electric hypercars, has received €500m from a consortium of investors led by Softbank Group based on a valuation of €2bn. The funds received will be, used to hire new staff, and to develop as well as produce batteries, software and other components for electric cars.

- Inspiration Mobility Group, the US-based financier of electric vehicles and builder as well as owner/operator of charging infrastructure secured new capital by an investment consortium (led by Macquarie Asset Management) to accelerate its mission of electrifying commercial fleets. The acquisition is a further step for Inspiration Mobility Group to underscore their commitment for sustainable technologies in the automotive sector.

- Raeuchle GmbH + Co. KG, the Germany-based automotive precision component specialist was acquired by Winning Group, a Czech-based provider of high precision parts for the automotive sector as well as construction engineering service. The transaction will enhance the financial situation of Raeuchle and will support the corporate strategy of Winning to become a diversified multi-technology company.

Selected Recent Global Automotive Bond Issuances Q2 2022

| Company | Date of Issuance | Amount (in €m) | Coupon (in %) | Yield (Latest) | Price (Latest) | Maturity Date |

|---|---|---|---|---|---|---|

| Continental AG | 27.06.2022 | 70 | 0.00% | (0.4)% | 100 | 28.07.2022 |

| Yokohama Rubber | 06.06.2022 | 93.8 | 0.58% | 0.7% | 99.2 | 04.06.2032 |

| Kubota | 02.06.2022 | 360.8 | 0.51% | 0.6% | 99.5 | 02.06.2032 |

| Goodyear Tire & Rubber | 28.04.2022 | 838 | 5.00% | 7.5% | 86.5 | 15.07.2029 |

Notes: 1) Deal value in Q3 2021 is driven by the Atieva/ Lucid Motors transaction (€23.5bn);

Sources: FACTSET, MergerMarket, AlixPartners, VDA, Market prospects, PwC

Download the Q2 2022 Automotive Newsletter to read more about the market performance.

Our deal experience

-

Clearwater Advisers

Adviser to the shareholders on the sale of a majority stake in Allgaier to Westron

View more -

Clearwater Advisers

Adviser to a Chinese state-controlled company on the sale of Innomotive Systems Hainichen to Mutares

View more -

Clearwater Advisers

Adviser to Kopernikus Automotive on the investment of a minority stake from Continental

View more -

Clearwater Advisers

Adviser to C2 Capital Partners on its investment in Grupo Simoldes

View more -

Clearwater Advisers

Adviser to Heitkamp & Thumann on the sale of Westfalia Metal Components to Vollmann Group

View more -

Clearwater Advisers

Adviser to Mahle on a corporate family rating

View more -

Clearwater Advisers

Adviser to Bridges Fund Management on its acquisition of Matrix Telematics

View more -

Clearwater Advisers

Adviser to Rolec Services and One Stop Europe on the sale to Sdiptech

View more -

Clearwater Advisers

Adviser to PMV and Finindus on the sale of Borit to Weifu

View more -

Clearwater Advisers

Adviser to BWI on receiving investment from Walden International

View more -

Clearwater Advisers

Adviser to Lander Automotive on its sale to GIL Investments Ltd

View more -

Clearwater Advisers

Advisers to the shareholders of Grupo Hispamoldes on its sale to Quarza Inversiones

View more -

Clearwater Advisers

Advisers to Abac Capital and its subsidiary Industrial Metalcaucho SL on the acquisition of Cautex

View more -

Clearwater Advisers

Adviser to KAP on its sale of Geiger Fertigungstechnologie GmbH to Zhejiang Tieliu Clutch Co., Ltd

View more -

Clearwater Advisers

Adviser to BENTELER Group on its sale of BENTELER Automotive Farsund to Chassix

View more -

Clearwater Advisers

Adviser to Faurecia on its acquisition of Jiangxi Coagent

View more