Automotive Newsletter Q1 2022

Download PDF

Overview of M&A activity

Russia's invasion of Ukraine is challenging the automotive industry and exacerbating already tense supply chain dynamics. Many manufacturers operate plants in both countries and rely on local suppliers, especially for wire harnesses and EV-related raw materials. In addition, the energy required for vehicle production and that needed to power vehicles has become noticeably more expensive as a result of the conflict. In the upcoming months however, the automotive industry is expected to recover from the wire harness crisis. Indeed, time-efficient and rapid capacity building in nearby countries will recoup the deficits.

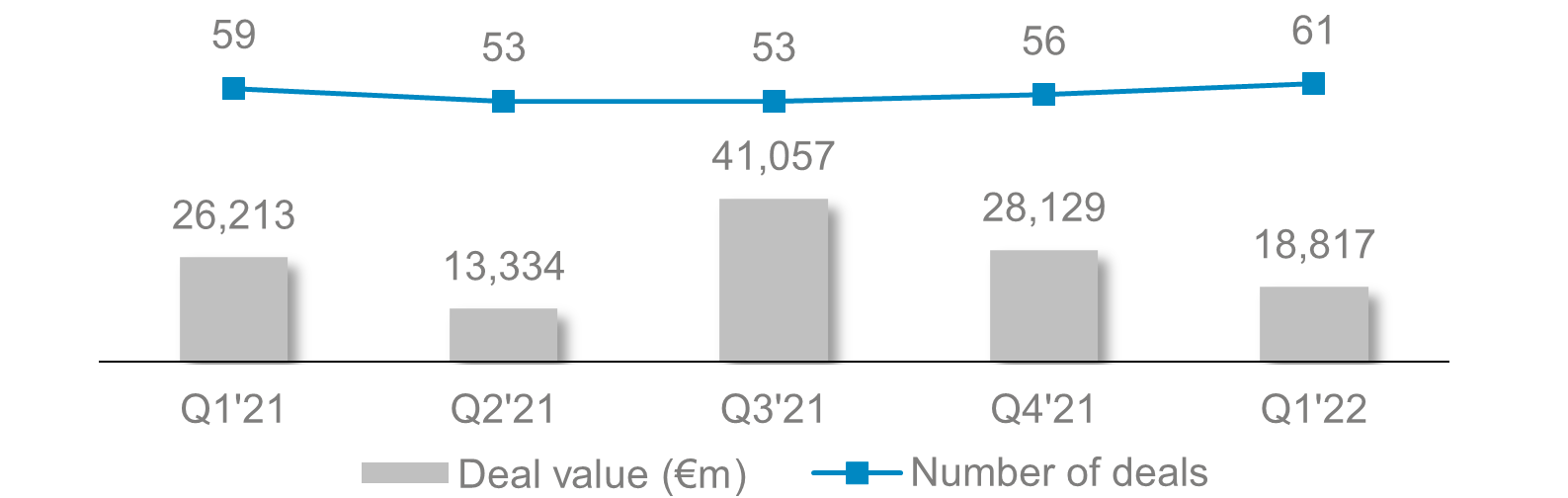

M&A activity slightly increased in Q1 2022 compared to Q1 2021

M&A activity slightly increased in Q1 2022 compared to Q1 2021, with a total of 61 completed transactions. However, the cumulative deal value has decreased in Q1 2022 (€19.3bn) compared to Q1 2021 (€26.2bn). Considerable activity in the areas of electromobility, autonomous driving, and fuel-cell technology continues to drive M&A activity in Q1 2022 with investments in companies such as H2 MOBILITY and EverCharge.

drivers for the anticipated upswing include the further development of autonomous driving

While valuation levels had been on a rise in Q4 2021 compared to Q3 2021, they have plummeted in Q1 2022. In Europe, EV/Sales, EV/EBITDA and EV/EBIT multiples decreased by 23.9%, 15.7% and 1.9%, respectively in Q1 2022. This trend is also observed in North America, albeit less pronounced, where EV/Sales, EV/EBITDA and EV/EBIT multiples decreased by 21.0%, 13.2% and 12.9%, respectively. Asia has also experienced a decrease in valuation multiples with EV/Sales, EV/EBITDA and EV/EBIT multiples dropping by 20.1%, 13.2% and 24.0% in Q1 2022, respectively.

Despite the challenges related to the Ukraine conflict in the first quarter, 2022 is a year full of potential, especially for e-mobility. Additional drivers for the anticipated upswing include the further development of autonomous driving such as level-3 vehicles, promising next steps in battery chemistry, as well as consumer preferences opting for more flexible forms of mobility access such as subscription models and micro-mobility solutions.

M&A Activity: Quarterly Comparison Q1 2021 – Q4 2022

Top M&A Deals Q1 2022

- H2 MOBILITY, a leading operator of hydrogen refuelling stations, has received investment from a consortium led by Hy24, the world’s largest clean hydrogen infrastructure investment platform. The investment will be used to upgrade the existing network and build new stations to meet rising hydrogen demand for commercial and intensive use vehicles.

- HELLA GmbH & Co. KGaA, the Germany based provider of lighting technology as well as electronic components and systems, was acquired by Faurecia S.A. (79.5% stake), the France based listed company engaged in providing automotive components. The combined group will focus on current automotive megatrends, including electric mobility, ADAS & autonomous driving, cockpit of the future, as well as lifecycle value management.

- Adler Pelzer Holding GmbH, the Germany based acoustic solutions developer to the automotive sector, was acquired by an Italy based family having interest in Italian automotive component manufactures (28.0% stake). The transaction further enhances the sound financial structure of Adler Group, with the objective to achieve the company’s ambitious growth plan.

- AutoForm AG, the global leader in engineering software for sheet metal forming simulation, was acquired by Investment firm Carlyle from private equity firm Astorg. Carlyle will help AutoForm accelerate its growth plan through the development of its existing software platform and through acquisitions, as well as by investing in the company's innovative product portfolio and business operations.

- Interplex Holdings Pte. Ltd., a key industry leader in future mobility power and signal connector technology, working closely with electric vehicle (EV) customers to develop proprietary solutions for EV powertrains, battery systems, autonomous driving, and other vehicle electrification applications, was acquired by asset manager Blackstone.

Selected Recent Global Automotive Bond Issuances Q1 2022

| Company | Date of Issuance | Amount (in €m) | Coupon (in %) | Yield (Latest) | Price (Latest) | Maturity Date |

|---|---|---|---|---|---|---|

| Faurecia | 20.01.2022 | 12 | 0.000% | -0.370% | 100.16 | 26.09.2022 |

| Aptiv PLC | 18.02.2022 | 644 | 2.396% | 3.639% | 96.69 | 18.02.2025 |

| Valeo SE | 23.02.2022 | 20 | 0.000% | -0.639% | 100.06 | 25.05.2022 |

| Continental AG | 30.03.2022 | 100 | 0.000% | -0.557% | 100.01 | 29.04.2022 |

Notes: 1) Deal value in Q1 2021 is largely driven by the PSA/ Fiat Chrysler transaction worth €19.1bn; 2) Deal value in Q3 2021 is driven by the Atieva/ Lucid Motors transaction (€23.5bn);

Sources: FACTSET, MergerMarket, EY, McKinsey & Company

Download the Q1 2022 Automotive Newsletter to read more about the market performance.

Our deal experience

-

Clearwater Advisers

Adviser to a Chinese state-controlled company on the sale of Innomotive Systems Hainichen to Mutares

View more -

Clearwater Advisers

Adviser to Kopernikus Automotive on the investment of a minority stake from Continental

View more -

Clearwater Advisers

Adviser to C2 Capital Partners on its investment in Grupo Simoldes

View more -

Clearwater Advisers

Adviser to Heitkamp & Thumann on the sale of Westfalia Metal Components to Vollmann Group

View more -

Clearwater Advisers

Adviser to Mahle on a corporate family rating

View more -

Clearwater Advisers

Adviser to Bridges Fund Management on its acquisition of Matrix Telematics

View more -

Clearwater Advisers

Adviser to Rolec Services and One Stop Europe on the sale to Sdiptech

View more -

Clearwater Advisers

Adviser to PMV and Finindus on the sale of Borit to Weifu

View more -

Clearwater Advisers

Adviser to BWI on receiving investment from Walden International

View more -

Clearwater Advisers

Adviser to Lander Automotive on its sale to GIL Investments Ltd

View more -

Clearwater Advisers

Advisers to the shareholders of Grupo Hispamoldes on its sale to Quarza Inversiones

View more -

Clearwater Advisers

Advisers to Abac Capital and its subsidiary Industrial Metalcaucho SL on the acquisition of Cautex

View more -

Clearwater Advisers

Adviser to Mühlhoff Umformtechnik on its sale to Fidelium Partners

View more -

Clearwater Advisers

Adviser to KAP on its sale of Geiger Fertigungstechnologie GmbH to Zhejiang Tieliu Clutch Co., Ltd

View more -

Clearwater Advisers

Adviser to BENTELER Group on its sale of BENTELER Automotive Farsund to Chassix

View more -

Clearwater Advisers

Adviser to Faurecia on its acquisition of Jiangxi Coagent

View more