EMS Newsletter Q2 2019

Download PDF

Executive summary of the EMS and ODM industry

The European EMS market grew to in excess of €31bn in 2018 with an expected annual growth of

c. 3% until 2022. Main growth drivers include continued digitalisation, Internet of Things (IoT), electrification and the expansion/roll-out of communication networks.

Increasing competition combined with market consolidation continues to increase price pressure. This is leading to the movement of production of low and medium volume/high mix electronic assembly from Western European countries.

Valuation level of EMS players worldwide

In December 2018, the valuation level of the EMS industry decreased to a level similar to mid-2016 (c. 5x EBITDA). The level recovered in April 2019 to above 6x EBITDA.

In general, global small and medium-sized EMS companies continue to show significantly higher valuation levels on average (c. EV/EBITDA ≥7x) in comparison to large EMS providers (c. EV/EBITDA 5x) and European players (c. EV/EBITDA 6x).

M&A activity in the EMS industry

Between mid-November 2018 and mid-June 2019, there have been 15 EMS transactions recorded with continued strong consolidation dynamics in the global market.

Clearwater International’s transaction highlight

CapitalWorks has agreed to acquire Libra Industries. Libra Industries, Inc. is a full-service solutions provider of engineered printed circuit board assemblies, electromechanical assemblies and electronic control solutions.

As a leading EMS contract manufacturer serving the medical, aerospace & defence, and industrial markets, Libra will complement another CapitalWorks portfolio company, GEMCITY Engineering and Manufacturing. GEMCITY is a contract manufacturer providing comprehensive manufacturing services for complex equipment used in the aerospace & defence, medical, packaging, and industrial markets.

Transaction highlights in the global EMS sector

- CapitalWorks has acquired Libra Industries. Libra Industries, Inc. is a full-service solutions provider of engineered printed circuit board assemblies, electromechanical assemblies and electronic control solutions.

- BB Electronics A/S, one of Scandinavia’s leading service companies in the field of electronics production, has acquired Czech company Wendell Electronics, with 130 employees and revenues in 2018 of €12.5m.

- PRIMEPULSE SE has acquired ETL Elektrotechnik Lauter GmbH, a company that manufactures electronic components. The company strengthens the EMS business activities of PRIMEPULSE Group which already consists of Katek Group and Steca Elektronik, Memmingen.

Overview of the European industry

The European EMS sector reached a market size in excess of €31.4bn in 2018 with forecasted CAGR of more than 3% until 2022. Main growth drivers include the expansion of the 5G network, IoT, ageing population and electrification of vehicles.

European market players are expecting the value of outsourced services in the electronics industry to grow in the next one to three years, due to growing demand of electronics and the maturity of the joint approach with original equipment manufacturers (OEMs) to outsource design and manufacturing services. Analysts forecast a 3-5% growth of outsourced electronic production in Europe with higher growth rates in the automotive and control & industrial sectors.

The strong competition and consolidation within the European EMS industry is set to continue. Key drivers for consolidation are economies of scale, access to and expansion of know-how and end-markets.

Shift of production towards LCC

Between 2000 and 2016 production in the EMS sector increasingly migrated from Western Europe to CEE/MENA. However, since 2016 there has been a slowdown in the migration of production from Western Europe.

Based on current market dynamics, which are characterised by high price pressure and competition, EMS providers will face the draw of migrating production to lower labour cost countries from Western Europe.

The latest hourly labour rates from China within the manufacturing sector are now broadly comparable with Bulgaria and Romania, which gives European EMS providers and OEMs less incentive to manufacture in China, unless there are other reasons, e.g. economies of scale or local market presence.

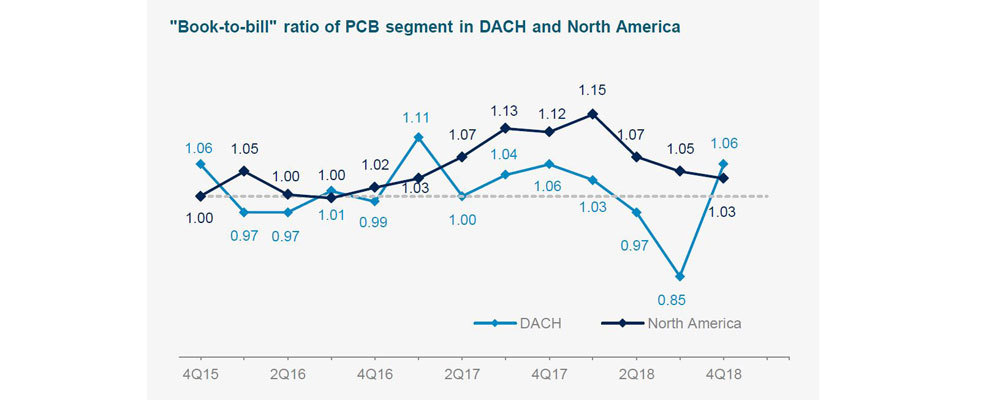

Quantitative outlook

The “book-to-bill” ratio, a ratio of orders received to the amount billed for a specific period, is an indicator of mid-term developments.

In the DACH printed circuit board segment, Q3 2018 experienced an all time low, however recovered by the end of Q4 2018 and increased from 0.85 to 1.06.

Growth trends in EMS end-markets

Digitalisation, IoT, the continued global expansion of Long-Term Evolution (LTE), and therefore the increased data usage, is forecast to fuel demand in EMS. Strong growth is expected in sectors including control & industrial, medical, automotive, and communication.

Industry 4.0 and IoT are driving improvements in wireless systems in home, manufacturing, office, and retail segments. The applications are becoming highly diverse, from AI/ VR introduction, smart lighting & building systems, robotics & automation, healthcare monitoring, all requiring extensive know-how.

The communication sector is also expected to grow due to the roll-out of 5G networks and further expansion of 4G in rural areas to upgrade slow download/upload speed in some regions.