To ‘V’ or not to ‘V’

Although the pandemic is continuing to cause huge disruption to the global economy, we are now seeing the beginnings of a recovery in China as it emerges out of the crisis. That makes it wise to start allocating at least some management bandwidth back to strategic planning and investment, especially as the business context in many sectors has been significantly reshaped. In this first post, partners Eduardo Morcillo, James Sinclair and Franc Kaiser look at the prospects for a global recovery.

At the start of this year we hoped, like most people, that COVID-19 would be a contained Far East crisis such as we saw with SARS and that a global pandemic was unlikely. Instead, today we are faced with a situation that far exceeds our worst-case scenario. The depth of the crisis is huge, and fires are popping up everywhere.

As China now emerges out of the crisis, the key questions from an economic viewpoint are just how deep and prolonged the global recession will be, and secondly what impact this will have on China’s own domestic recovery.

Dark clouds amassing

In terms of the first question it is almost impossible right now to know exactly how deep the global recession will be, and what shape the recovery will take. However, in the medium term a number of dark and very large clouds continue to hover above us.

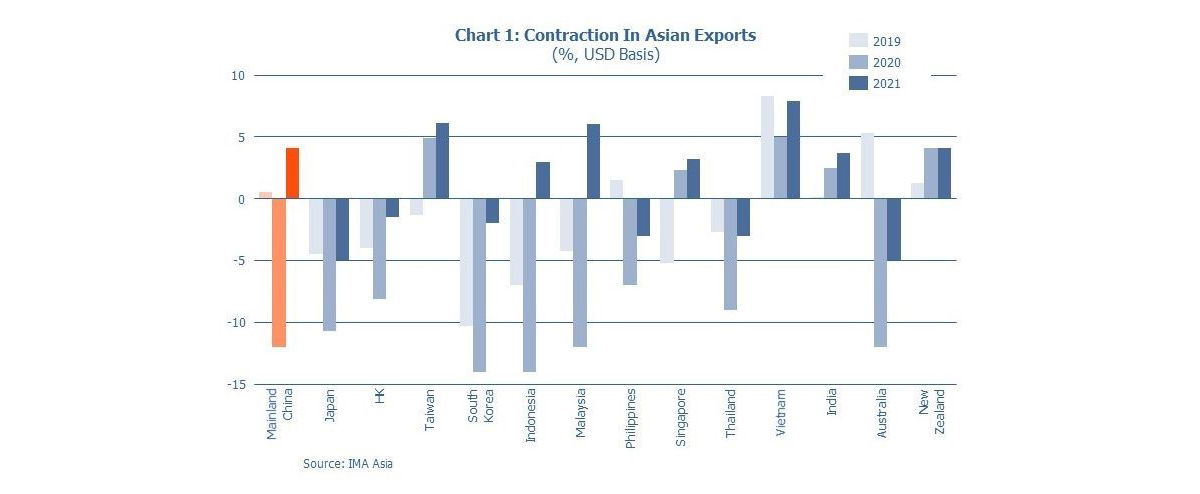

Firstly, our view - based on the present trajectory of the virus - is that it could take most countries two to three months longer than China to emerge from the worst of the crisis, and that takes us well into the summer and maybe the autumn. Eliminating COVID-19 worldwide will take longer - and be deeper - than in China.

A second cloud is that the longer this crisis lasts, the greater the risk of a credit crunch. Many companies are highly leveraged, following a decade of low interest rates and cheap money. The COVID-19 outbreak is now exposing this imbalance in the financial system.

With the drop in revenues, spike in borrowing costs, and difficulty in rolling over debt, a surge in corporate defaults and bankruptcies looms. We will see whether intervention by central banks and national governments is sufficient to ward this off and avoid the same squeeze on bank liquidity that we saw during the global financial crisis.

fears are growing that the relationship is approaching breaking point

The third cloud is political. The China-US relationship was stressed prior to the outbreak, but fears are growing that the relationship is approaching breaking point. The deeper the impact on the US economy and society, with the US election nearing, the more the motivation for Washington to direct blame towards Beijing. Meanwhile in China, there is a swelling in confidence in the Chinese model, and belief that China will continue to rise in the global order. With pressure on both sides, and flash points inevitable, we can only hope for political restraint.

Silver lining in China?

Amid this gloom there are, however, rays of light. We have learned from conversations with CEOs in China over recent weeks that, not only are international companies ramping up production in the country, but some are even planning to expand capacity over the coming months. The reason is that, with most western nations in lockdown, China-based plants might be the only viable supplier to the global economy. This concentration of manufacturing activity in China could, for numerous supply chains, help offset the decline in global demand.

The recent downturn will also bring a new wave of corporate activity to continue the consolidation trend of the past few years. Many Chinese companies will seek investors/buyers, as the long-term challenge of remaining competitive in China are combined with short-term cash flow pressures. True, some sellers will try to hold out for better valuations, and some potential buyers may not have financing available. However, a good number of international companies will be active, particularly those whose headquarters recognize the and support this time to pursue growth in China.

China is still well positioned to be one of the main drivers of the global economy in 2020.

Chinese economic recovery

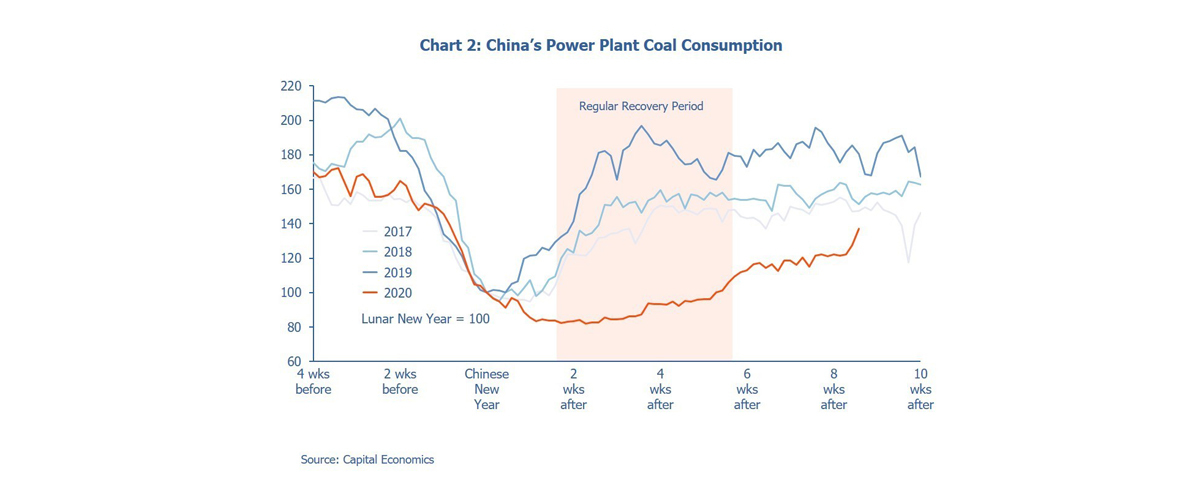

Taking a more detailed look at economic prospects for China, in our view, the country is still well positioned to be one of the main drivers of the global economy in 2020. Their forecast is for ~3% domestic growth this year, albeit considerably down on initial projections of around 5~6% at the time COVID-19 first struck China. This would make for a moderate recovery, closer in shape to a ‘V’ (quick) than ‘U’ (prolonged) or ‘L’ (weak).

The recovery will be driven both by the resumption or regular economic activity as well as government stimulus. Consumer demand will play an important role, as the outbreak has done little do damage confidence, jobs or salaries. Meanwhile, the Chinese economy is full of companies ready to make up for lost time, or impatient for a fast restart as their survival is on the line. And given the significance of the 2020 targets to the Chinese government, Beijing will spare no effort in cranking up the machine.

Targets set in stone

2020 is a politically important year for China’s leadership. It marks the end of the 13th five-year plan (2016~2020), by which time Beijing promised a “comprehensively well-off society”.

China's policy space is more limited than during the global SARS outbreak or global financial crisis. For instance, its higher debt levels today pose the risk of lower growth further down the road, while there is a diminishing pool of good infrastructure projects with which to stimulate activity. Inflation may also be pushed higher by the limited supply of certain goods. Nonetheless, Beijing still has significant fiscal and monetary policy levers to pull, and the stimulus will be better targeted.

China's policy space is more limited than during the global SARS outbreak or global financial crisis.

China’s central bank will pursue an expansionary monetary policy (a) by relaxing the bank reserve requirement ratio for commercial lenders to unleash long-term and targeted funding to the economy, and (b) by considering cutting interest rates further at an appropriate time. Beijing may also allow the RMB to depreciate and thereby help stimulate demand.

Meanwhile, China will enter a period of fiscal easing that may include (a) further tax cuts (b) coupons or subsidies on specific goods and services to stimulate consumption (c) targeted support for certain industries, especially in public health and healthcare, advanced industry, and communications networks (d) subsidies for SMEs, such as reduced rent and social security commitments, as well as debt relief (e) bringing forward existing infrastructure development plans, especially in the worst-hit regions.

Next time

In the next posting we look at the lessons the rest of the world can learn from the Chinese experience of COVID-19.

Blog Series

1. Recovering from COVID-19: to ‘V’ or not to ‘V’

2. Recovering from COVID-19: lessons learnt from China

3. Recovering from COVID-19: action points for industrial players

4. Recovering from COVID-19: action points for retail and brands

5. Recovering from COVID-19: the M&A opportunity