Value-Added Distributors Clearview

Download PDF

Market trends

Value-added distributors (VADs) are becoming increasingly prevalent across a broad range of sectors including business supplies, construction, energy, consumer products, transportation and agriculture.

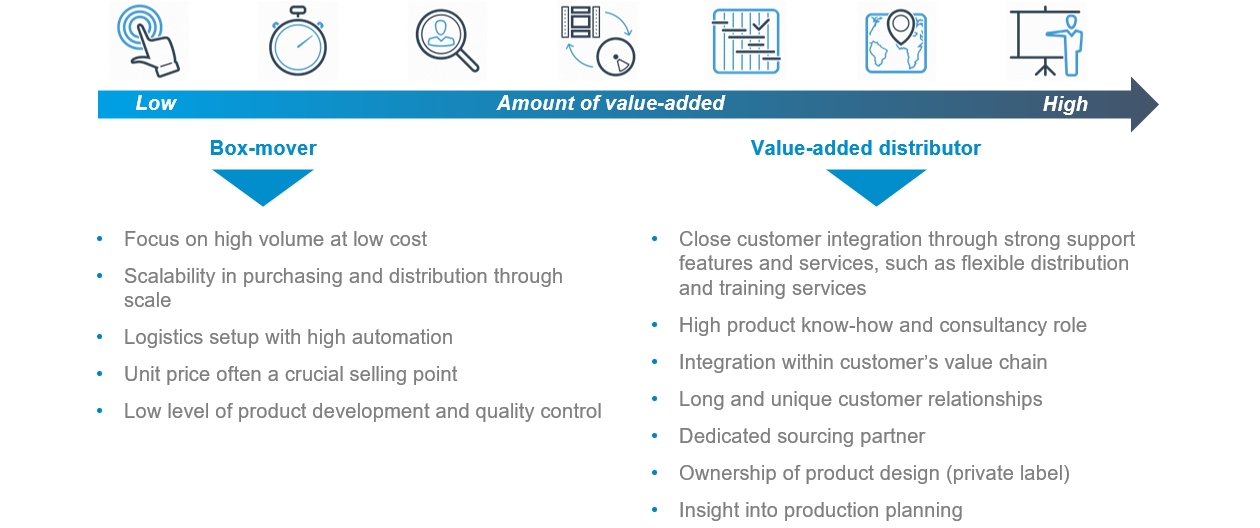

Whilst the market for VADs is broad, there are several common characteristics that typify a VAD in terms of strong customer relationships, specialist knowledge across niche product categories and the ability to quickly source the right products for the customer. VADs are distinguished by:

- Offering an effective sales channel for manufacturers

- Providing significant value-added services for end-users over and above the sale of products

- Integrating into customer's value chain, often acting as a business-critical sourcing partner

- Acting as a consultant with extensive product knowledge and technical expertise

Successful VADs are already adapting to ongoing trends. The market for VADs is being driven by three notable trends:

Digitalisation: A large number of VADs remain in the early stages of the digitalisation process. Successful VADs exploit the growing potential of digitalisation. For example, in the form of inventory management systems, product information management (PIM), logistics planning, automation or e-commerce.

Increased need for documentation: Documentation needs and regulations for certain product types place greater demands on sourcing and cooperation between distributor and manufacturer. VADs provide a valuable service to end-users by providing easily accessible documentation, serving as another way to differentiate themselves from traditional distributors and online competitors.

Own brands: The use of own brands among VADs, often in the form of private label-sourcing, continues to grow. This opens up the possibility of product tailoring according to specific customer needs and serves to further deepen the sourcing relationship.

Types of distributors

M&A activity

As VADs gain momentum there is a growing appetite for consolidation. This is manifested by active acquisition strategies from established distributors as well as industrial conglomerates and financial investors seeking bolt-on acquisitions for existing portfolio companies and new stand-alone platform investments.

Multiple rationales are driving acquisition interest

Acquisition rationales such as diversification of the customer portfolio, increased know-how in a product niche, acquisition of talent and increased geographical presence are some of the factors that buyers cite as driving M&A activity. Three rationales are particularly prominent:

Expanding product coverage: Providing specific know-how and product knowledge enables the buyer to cover the entire product spectrum demanded by the customer, and act as a "one-stop shop" for the customer, reducing competition and strengthening the relationship.

Internationalisation: International customers increasingly want to engage with VADs who are able to operate across borders, providing the same high service level and delivery security across multiple territories negating the need for multiple distribution partners.

Scale: A significant factor for distributors, regardless of the amount of value-add, is the negotiating position between supplier and customer. As VADs are often dependent on a few large customers, there is a risk element that can be diversified by becoming part of a larger international acquisition player due to scale.

Acquisition interest comes from several types of players

The acquisition interest in VADs typically comes from a number of angles.

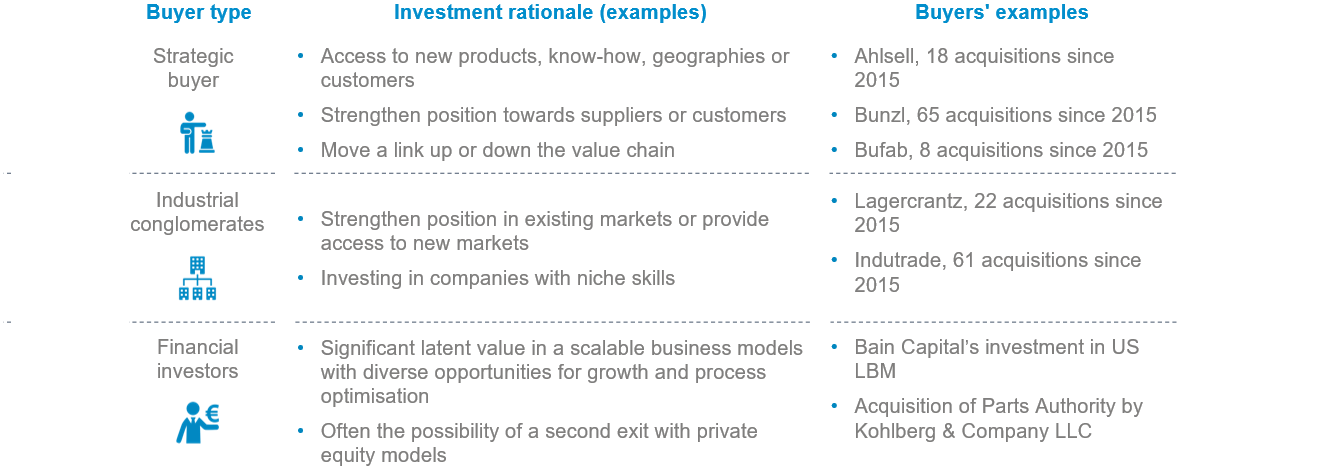

Strategic players: Much of the consolidation is driven by well-established distributors, who have achieved a position in the market where organic growth is not sufficient and therefore resort to acquisitions as a growth driver. However, strategic players can also be seen in the form of manufacturers who want to enter the value chain and gain greater control over a sales channel, as well as customers who want to move back into the value chain.

Financial investors: VADs have also drawn the interest of financial players, with several notable successful cases. Financial investors include both private equity funds and family funds with different investment horizons that see good opportunities to grow the business. For example through acquisitions and strategic development.

Industrial conglomerates: International industrial conglomerates are increasingly adopting the private equity mindset, diversifying operations across a range of services and markets, supported by a significant operational infrastructure and the potential to benefit from enhanced scale, synergies and cross-selling.

Buying interest in VADs comes from multiple angles

The primary buyer groups

Prior to sale considerations

The majority of company sales depend on several factors, some of which are specific to distribution companies as well as general factors that apply to all types of businesses. Vendors should consider a range of internal and external factors including financial maturity and timing as well as the evolution of the underlying market and the presence of competitors and potential investors.

VAD specific factors to consider include the relative position within the value chain, the degree of value-add, how good inventory management is and the degree of digitalisation. External factors largely relate to customer and supplier dependency, competitiveness and spend.Factors that should be discussed and assessed in the context of sales maturation

Transactions experience

Clearwater International has extensive experience in advising VADs across a range of end markets including industrials & chemicals, healthcare and consumer.

Case study

Clearwater International advised on the sale of HT Bendix, a leading C-parts supply chain partner to the furniture and kitchen industry, to Swedish Bufab. The company generates annual sales of approximately €45m in Denmark, Germany, the UK, France, Poland and the Baltics, and has achieved continuous and profitable growth since the company was acquired by management and Industri Udvikling in 2012.

1975 — A/S Herning Trælast is established and starts selling tools and fittings to the professional market and industry. In 1991, DT Group merges the company with BENDIX Tømmerhandel A/S and creates "HT BENDIX".

1990s — HT BENDIX sharpens its focus towards exclusively selling fittings to the furniture, kitchen and woodworking industries, leading to a decade of continuous annual growth records and expansion of the operational setup with automatic warehouse management systems and larger facilities.

2012 — DT Group sells HT BENDIX to management with the backing of the Danish private equity fund Industri Udvikling.

2012 - 2019 — A new era of professionalization and continuous annual revenue growth follows the ownership change driven by the independent and value-focused management style.

2018 — Following a general strengthening of the management team as part of a long-term strategic plan, Clearwater International were appointed to advise on the potential sale of HT BENDIX.

2019 — HT BENDIX is sold to Swedish Bufab, a publicly traded value-added distributor, ensuring attractive growth synergies for both companies.