Q4 2019 summary

Download PDFThis report identifies key themes driving European Private Equity (PE) deals’ EV/EBITDA multiples on a quarterly basis. The objective is to assist PE investors in understanding drivers behind value trends across regions and sectors, leading to good investment opportunities.

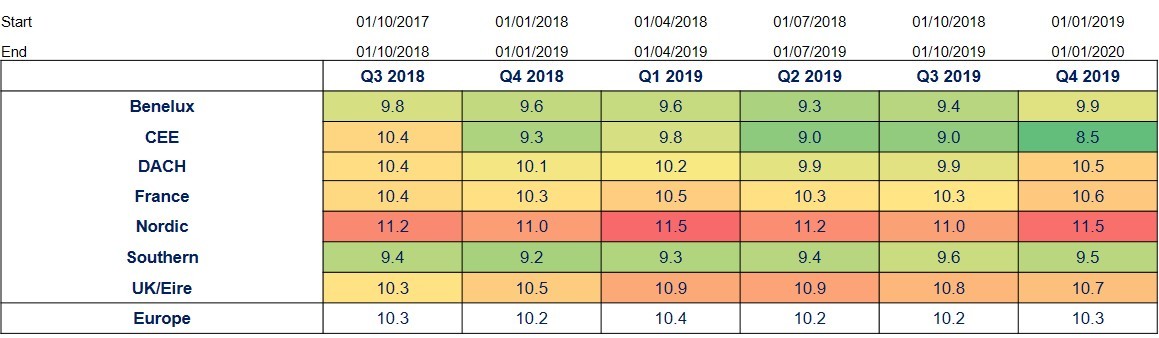

For the first time since Q1 2019, this quarter saw a slight increase of just over 1% in average multiples paid in PE backed transactions throughout Europe when compared with the previous quarter. This reverses the trend of gradual decline in average multiples since Q1 2019.

In line with the last two quarters, the Nordic region again saw the highest average multiples paid in PE transactions, also up nearly 5% on the previous quarter. Average multiples in the region have consistently been over 10x since Q3 2018.

Following a steady multiple decline through 2019 the DACH region saw the largest increase against the previous quarter with a jump of over 6%. Benelux and France saw more modest increases of 5% and 3% respectively.

The UK and Ireland was the second hottest region in terms of multiples, up 1% on the same quarter in 2018 but down 1% on the previous quarter. Since Q4 2018, average valuations in the region have been relatively stable, varying by less than 0.5x in the period.

There was a sharp decline in valuation in Central and Eastern Europe in the quarter, with a decline of nearly 6% when compared to the previous quarter, and 9% when compared to the same quarter in 2018. Multiples were also the lowest of any of the regions in our analysis.

The Southern region also saw a decline in multiples when compared to the previous quarter, despite an increase of over 2% against the same quarter in the previous year. Average multiples in the region have been fairly consistent since Q3 2018.

For the first time since Q4 2018, the financial services sector didn’t deliver the hottest average valuations, despite a modest increase in average multiples of 1% on the previous quarter. The sector saw the second highest average multiples, despite being slightly lower than peak valuations of over 12x in Q1 and Q2 2019.

The highest average multiples for the quarter were seen in the TMT sector and the sector also delivered its highest average multiple for the quarter since Q1 2019

The healthcare sector was the next richest sector in terms of valuation despite a small decrease in average multiples from the previous quarter. The sector delivers consistent valuations with the range of averages shifting by no more than 0.5x over the last six quarters.

Modest growth was also seen in industrials and chemicals in comparison to the previous quarter and the same quarter in the previous year.

The consumer sector saw a slight reduction in average multiples for the first quarter since Q4 2018. Prior to Q4 2019, multiples steadily increased by an average of 1% per quarter.

The second hottest deal range was €500m-€1bn for the third quarter in a row, despite being nearly 5% down on the previous quarter. For the fifth quarter in a row, the €250m-€500m was the third richest deal range, being up over 7% on the previous quarter. The sub €250m categories all saw modest growth against the previous quarter and the same quarter for the previous year, with the €50m-€100m range delivering the lowest average multiples of any category. In this quarter, the Multiples Heatmap focuses on trends seen in the DACH region and the business services sector.