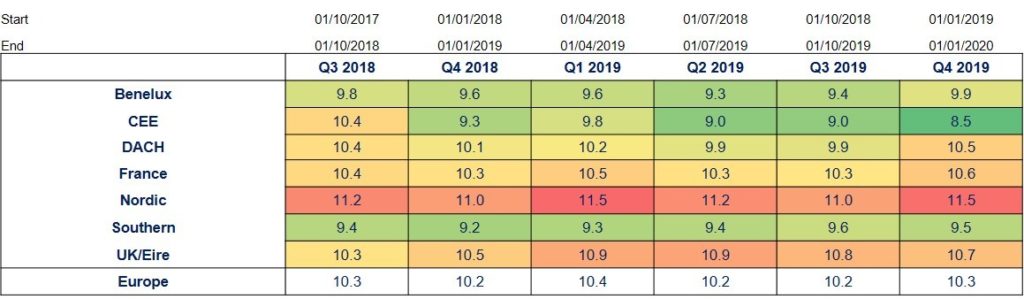

Irish market overview

Download PDFIn the past five years, Irish M&A has seen unprecedented activity, and with that, increasing entry multiples. Illustrating the buoyant sellers’ market, the value of buyouts in 2019 reached €3.5bn, the highest level since 2006, according to Unquote Data.

Curtin points out the strength of the economy has contributed to the high-multiples environment. “Banks are in a stable position so there’s a high availability of capital” says Curtin. Alternative debt firms also contribute to the level of capital available.

With the growth of entry multiples in the Irish market and the amount of dry powder in private equity coffers, Curtin says he’s seen fund managers outbid trade buyers in several processes. “Normally a large trade player would be able to pay more for the synergies they can achieve with an asset but there’s a lot of capital available and PE buyers are going to pay up for quality assets, particularly with contracted revenues,” he says.

In addition, Ireland has caught the attention of international players. UK private equity firms particularly are looking at Ireland as an alternative to UK-based investments. Curtin says: “There are clearly high-quality assets on offer.”

International attention

Clearwater has also sold several assets to international PE backers. These include the sale of KB Associates to ECI and Version 1 to Volpi Capital. Other international investors in Ireland in 2019 include Waterland Private Equity, Charterhouse Capital Partners and Blackstone. Both Waterland and Blackstone have offices in Dublin.

Curtin says spending time in Ireland can be a way to combat high multiples. Building relationships with entrepreneurs and management teams and educating business owners on private equity can be the key to clinching a deal. “There have been a number of bilateral deals done by smart international fund managers who have spent the time here” says Curtin.

Additionally, vendors are beginning to choose acquirers on factors other than the price they can offer. Certainty of the deal being executed and offering committed funding can be very important in a sales process. Management teams also consider the relationship they have with their acquirers as vital. “From a PE perspective, you’re on a journey for 3-7 years. You need to be able to work with each other,” says Curtin.

Sector perspective

As is the case with the rest of Europe, technology companies in Ireland are commanding the highest multiples of any sector. In Q4 2019, the average entry multiple for TMT reached 12x, beating financial services at 11.9x. Says Curtin: “There are companies that are not making profits that are achieving 6-8x revenue multiples upon sale.”

Across Europe, the average entry multiple in the industrials sector reached 7.5x EBITDA in Q4 2019, the lowest performing sector. Says Curtin of Irish industrial companies: “Low-margin, industrial businesses with no recurring revenue will have difficulty achieving high multiples. Many of them are domestic businesses so they’re difficult to scale and grow internationally.”

The general sentiment for activity in 2020 is highly positive. “Activity in Q4 fell off a little bit, but when the new year kicked off it was all systems go. We have a very strong pipeline.” Curtin expects multiples to remain steady in 2020. “It wouldn’t be a good thing for them to increase significantly, from the levels seen in 2019. It was a blockbuster year.”