European overview

Download PDF

Our quarterly report identifies the major themes driving EV/EBITDA multiples in European private equity (PE) deals. The objective is to help PE investors understand trends across regions and sectors, leading to better investment decisions.

The value of PE-backed transactions in Europe surged to an all-time high in Q2 2022 – despite tough macroeconomic conditions

The value of PE-backed transactions in Europe surged to an all-time high in Q2 2022 – despite tough macroeconomic conditions and mounting geopolitical turbulence.

Deep reserves of liquidity and fierce competition for high-quality assets contributed to a quarterly deal total of €83.6bn, a 32% increase from Q1. TMT led the way, clocking up deals worth €22.7bn, the sector’s highest quarterly total since records began.

While overall value was sharply higher in Q2, deal volume was down 3% from the previous quarter, with a total of 283 transactions. Against this background, the average long-term EV/EBITDA multiple for European PE transactions climbed to its highest level on record.

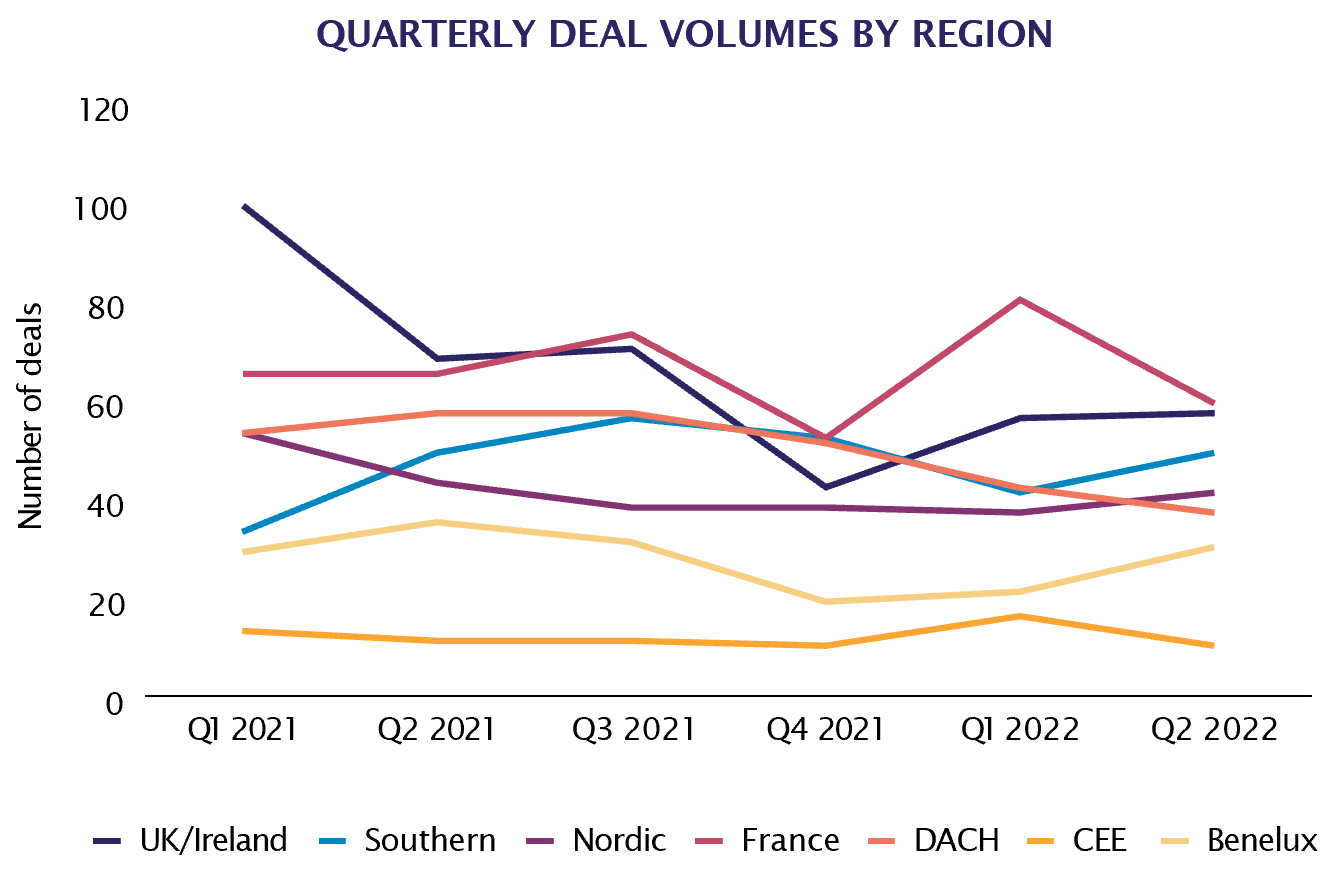

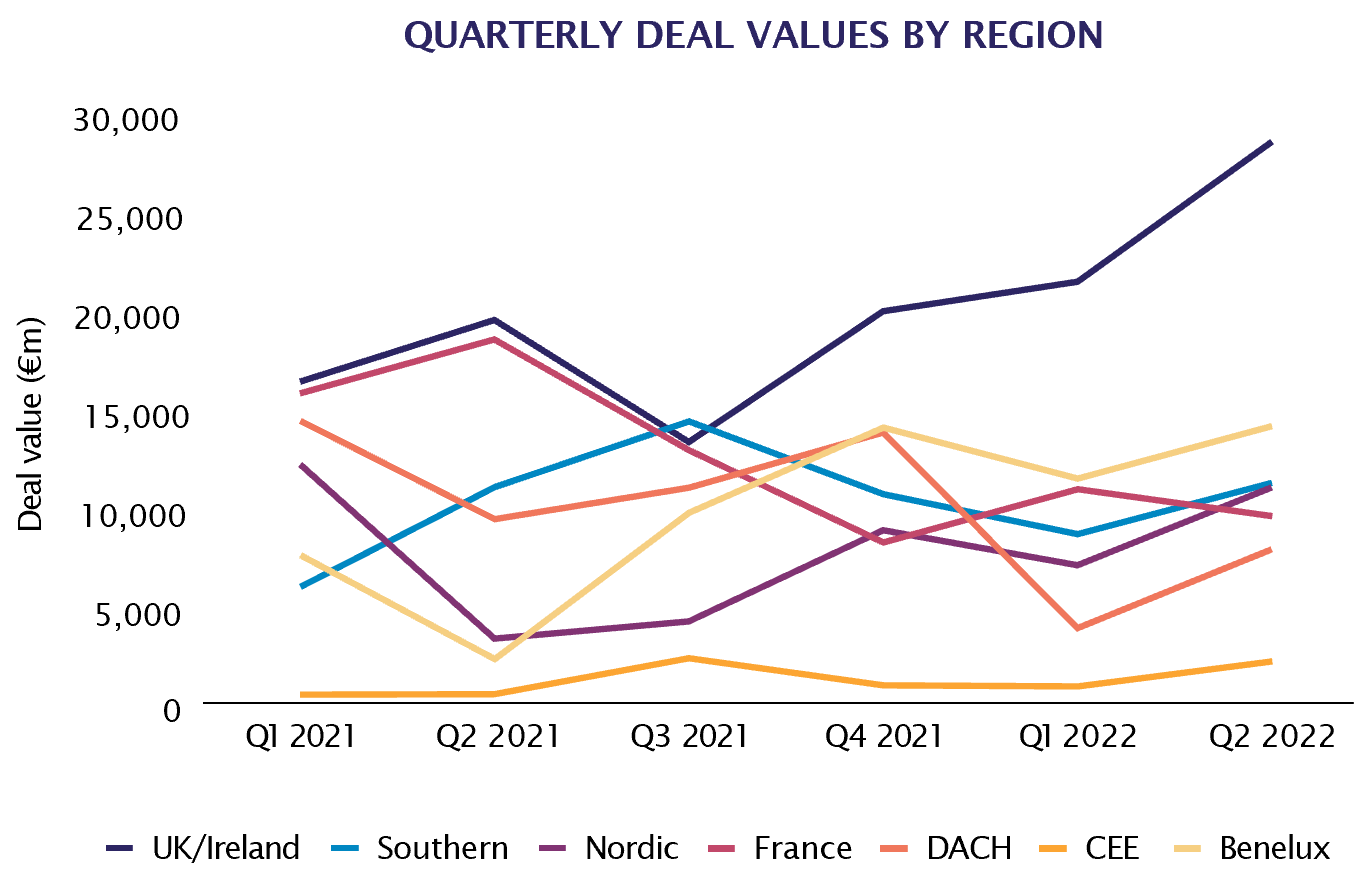

Regional overview

The UK and Ireland has long been Europe’s top-performing PE market, and Q2 2022 was no exception. While deal volume was solid rather than spectacular, the quarterly deal value – €28.3bn – is a new pan-European record. Meanwhile, Q2 marked the eleventh consecutive quarter in which the UK and Ireland’s deal multiple either rose or stayed the same. No other geography has an unbroken record of this length.

Despite resurgent inflation, jittery markets and an anticipated eurozone rate rise (which materialised at the beginning of Q3), most regions saw strong performance in deal value terms in Q2, with only France posting a decline. That said, France was Europe’s biggest deal generator in the quarter, albeit only just, recording 59 deals compared to the UK and Ireland’s 57.

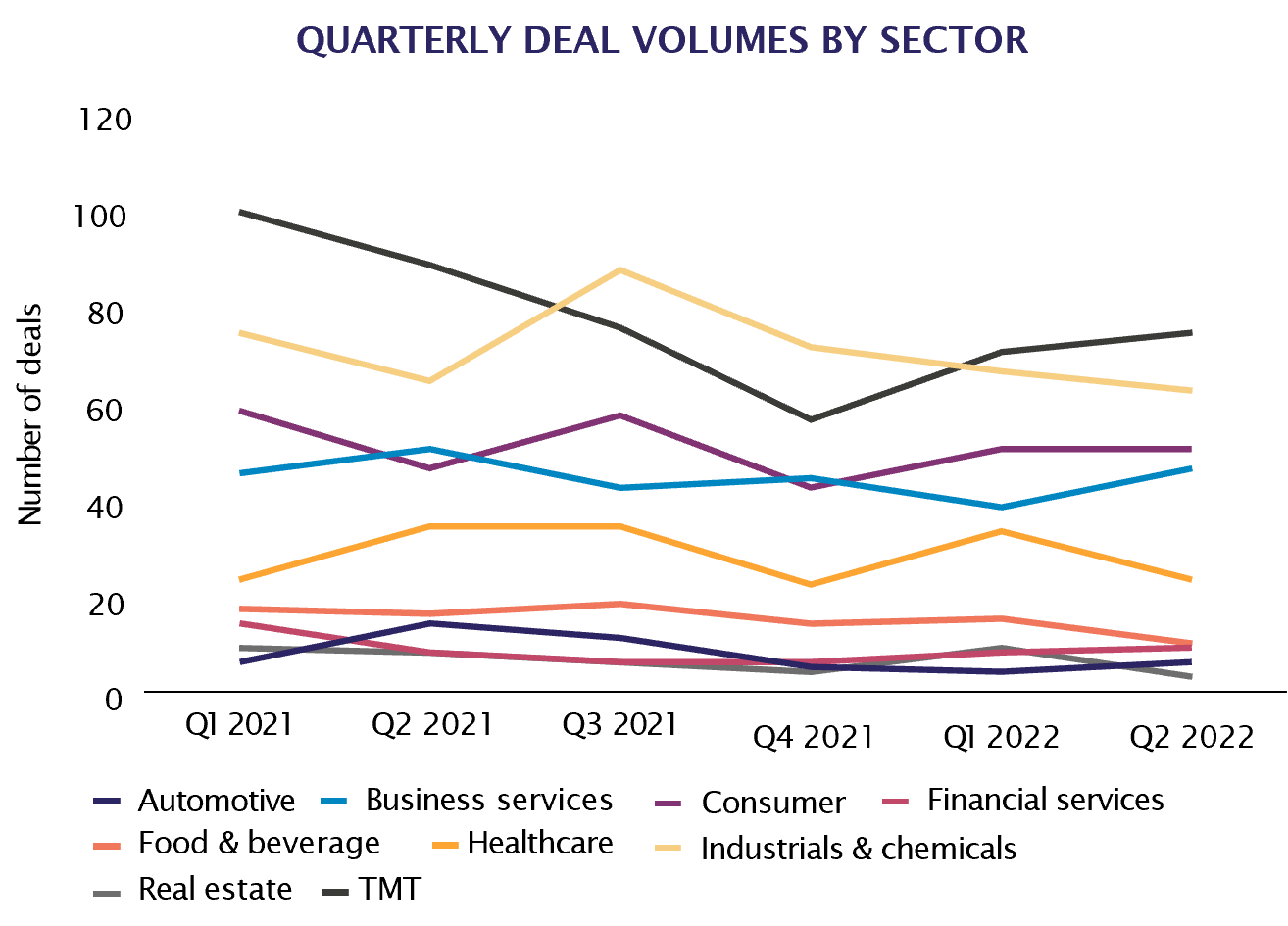

Sector watch

The stars aligned for TMT in Q2 2022. The sector achieved the highest quarterly volume (74, accounting for more than a quarter of the regional total across all sectors), in addition to the greatest deal value (27% of the total) and the biggest long-term deal multiple. On top of this, TMT generated the largest deal of Q2: an investment by GIC, Singapore’s sovereign wealth fund, in The Access Group, a UK-based business management software specialist.

Industrials & chemicals and the business services sectors saw their long-term deal multiples rise in Q2. The former recorded slighter fewer buyouts in Q2 (62) compared to the previous quarter (66), though these transactions were worth a great deal more in aggregate – €16.9bn, more than double the output achieved in Q1 (€7.6bn). The business services space is also booming, as Clearwater International partner Rob Burden describes in the ‘Sector focus’ chapter of this report.

That being said, the quarter also saw deal multiples in some sectors easing from the all-time highs achieved in Q1 – notably financial services and food and beverage, both of which retreated by just over one turn of EBITDA.

The figures posted in the consumer sector also withdrew somewhat, by half a turn of EBITDA quarter-on-quarter, although the industry did record higher aggregate value in Q2 (€10.8bn) than in Q1 (€6.5bn) on the same number of transactions (50 in each three-month period). Europe’s mounting ‘cost of living’ crisis and inflationary pressures may be putting a squeeze on consumers’ budgets, but deals are evidently still to be made in the space.

Selected Clearwater International private equity transactions from the last quarter

-

Clearwater Advisers

Adviser to the shareholders of OCU Group on its sale to Triton Partners

View more -

Clearwater Advisers

Adviser to Klaravik on its majority sale to TBAuctions

View more -

Clearwater Advisers

Adviser to the shareholders of LDC on the sale of Littlefish to Bowmark Capital

View more -

Clearwater Advisers

Adviser of A&M Capital Europe on the acquisition of the majority stake in Carton Pack, a portfolio company of 21 Invest

View more -

Clearwater Advisers

Adviser to Mountain Village on the sale to Equip Capital and Vendis Capital

View more -

Clearwater Advisers

Adviser to H&MV on its investment from Exponent

View more -

Clearwater Advisers

Adviser to Vitae Naturals on its sale to Kensing

View more