OEM strategies

Announcing plans to launch a public ride-sharing service in several cities that use fully self-driving cars by 2019, General Motors recently described self-driving cars as “the biggest thing since the internet”.

For OEMs such claims are fully justified. Precisely how they match consumer needs with autonomous driving solutions, while overcoming public scepticism about relinquishing control of vehicles, remains a key question. Which business models will win in this new landscape?

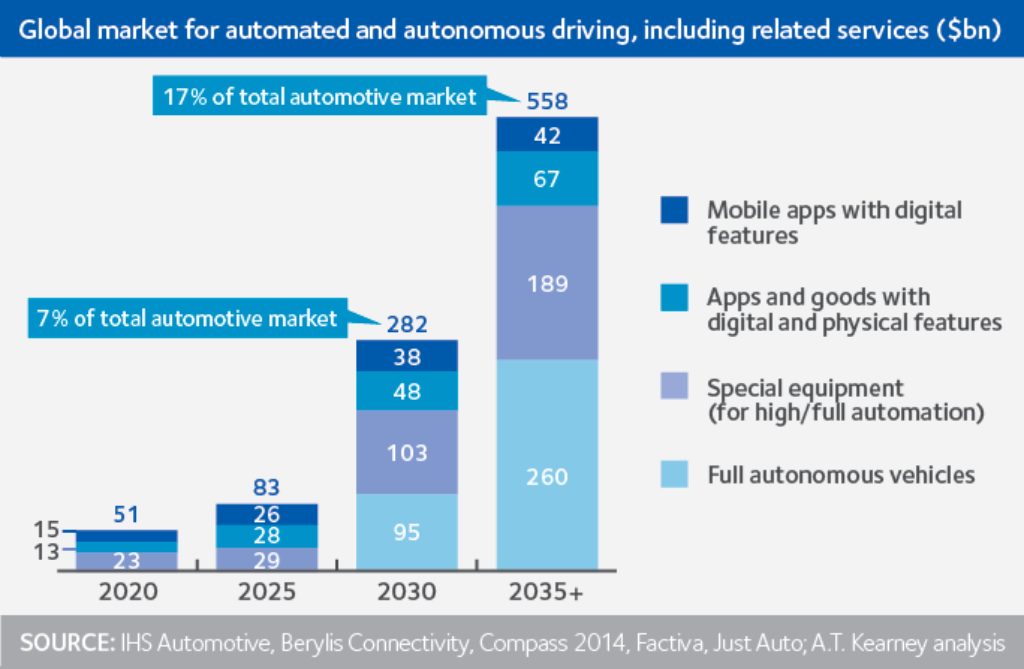

A.T. Kearney1 predicts that although it will take up to 20 years for fully autonomous driving to emerge, not all OEMs will get a piece of the market and it is dangerous to assume that the sheer size of the market will guarantee that everyone is a winner.

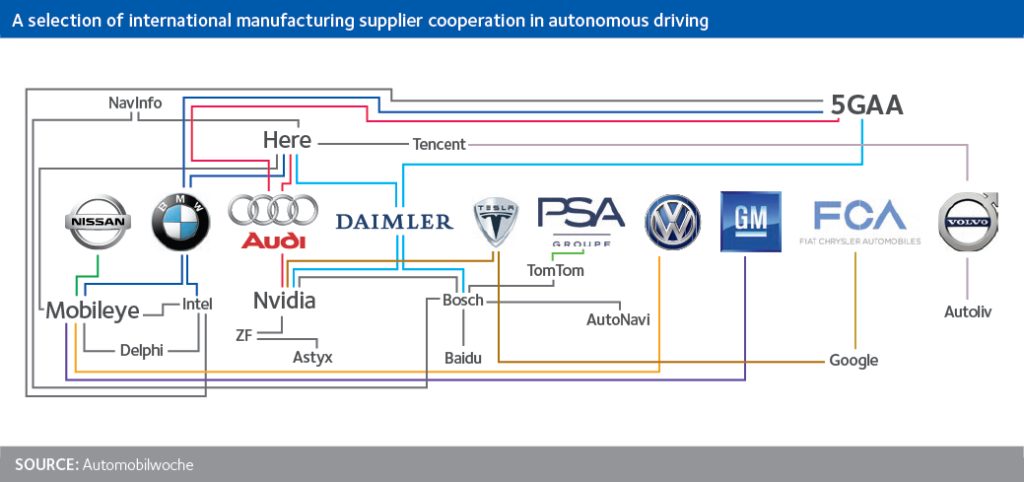

In particular it thinks that the existing ‘pyramid’ value chain in the automotive industry will be replaced by more of a hub-and-spoke arrangement (see above). Compounding the challenge is that nearly all participants in the other spokes are multi-billion dollar companies with strong research and development teams, regional or global market leading positions, and have “an appetite for large, game-changing growth opportunities”.

Against this backdrop OEMs are having to think hard about which players they should be partnering with. As the chart below shows, they are in a scramble to secure tie-ups with the partners that they think they will need to gain market share.

A good example of a deal earlier this year saw chipmaker Nvidia partner with Uber, VW and China’s Baidu. Uber will use Nvidia’s chips for its artificial intelligence (AI) computing system in its fleet of self-driving cars, while VW will use the Nvidia Drive IX platform to help develop its next set of cars.

OEMs also need to take on board the impact that AVs and changing consumer habits will have on their bottom line. For instance, one of the reasons why there has been so much corporate activity around the ‘robo-taxi’ market is that observers think this could be one of the first areas to really see the impact of AVs as more consumers seek connected and shared driving options.

When we spoke to leading AV expert Professor Dr Hans Christian Reuss, from the Research Institute of Automotive Engineering and Vehicle Engines in Stuttgart, he said AV is a very complex subject for OEMs because it cannot be considered separately from the topics of electrification of the drives and networking of the vehicle’s functions.

He adds: “A particular challenge is safety as for vehicles with automation levels 3 and 4 billions of kilometres of testing are required, and this protection can only be fulfilled with virtual test procedures such as ‘Virtual Integration and Test’ or ‘Hardware-in-the-Loop’ testing of automation functions and driving simulation. Due to the enormous importance and the interdisciplinary nature of autonomous driving there will be great demands on the education and training of engineers.”

1: A.T. Kearney – How automakers can survive the self-driving era