Market overview

Specialised Engineering Service Providers (ESPs) have always played a role in the automotive industry however, as a recent report notes1, in the past they were mainly used for specific tasks such as creating drawings, designing components and modules, calculating specifics, and for conducting testing procedures.

Today the picture is very different as OEMs outsource a huge range of engineering activities to ESPs, including the development of systems and derivatives, and even complete vehicles. They have also sought ESP support for services such as quality assurance, supplier and project management, and for training programmes.

In turn, ESPs now need the capability to work on completely new development projects which demand expertise in all aspects of product development. As the report concludes, the ESP will “make or break” the success of an outsourced product development project which makes it imperative for the OEM to carefully assess the competencies of an ESP partner.

Services

Engineering services across the automotive sector break down into five core areas2:

- Design services - design and surfacing, virtual reality, design modelling

- Simulation - crashworthiness, occupant safety, structural add-on parts, stiffness/vibration, fluid dynamics

- Modelling/ Rapid tech - CAD/CAM, milling technology, gauge building, toolmaking, measuring technology

- Testing - interior/exterior testing, engine chassis and tank system, vehicle safety, acoustics, electric mobility, vehicle construction

- Engineering services - project management, quality management, process validation, logistics

Market growth

The overall benefits for individual ESPs depends on the degree of specialisation that they can offer to OEMs and the types of services that they provide. For instance, whether they focus on interior/exterior engineering as opposed to powertrain engineering.

That said, the need for R&D efficiency among OEMs will require them to outsource all non-core competence tasks and lead to the outsourcing of ever larger work packages. One forecast3 predicts that the engineering services market will increase from €11.1bn in 2017 to €18.3bn by 2023 at a CAGR of 8.7%, while another4 predicts that the global automotive ESP market will see a CAGR of 6.3% between 2018-2022.

Research and development

R&D spending in the automotive industry will continue to rise as OEMs need to invest in new technologies.

R&D spend in the automotive industry

Source: 2018 EU Industrial R&D Investment Scoreboard

| Company | R&D spend 2017/2018 (€bn) |

|---|---|

| Volkswagen | 13.14 |

| Daimler | 8.66 |

| Toyota Motor | 7.86 |

| Ford Motor | 6.67 |

| BMW | 6.11 |

| General Motors | 6.09 |

| Honda Motor | 5.40 |

| Fiat Chrysler | 4.28 |

| Nissan Motor | 3.66 |

| Denso | 3.30 |

Much of this spending is in Europe where in 2016/17, 24% of all R&D spend5 went on the automotive sector, while in Asia the automotive sector accounted for 19% of R&D spend. VW is by far the largest R&D investor in the sector. In late 2018 it announced6 that, in order to accelerate its pace of innovation, it would increase its investment in R&D in the areas of digitisation, autonomous driving and electric mobility to €44bn over the next five years, up from an initial estimate of €34bn.

At present, VW the company has six battery-powered models in its product range, but by 2025 it has plans for more than 50 models and to produce approximately a million electric cars annually. VW has reached strategic supply agreements with a number of Korean and Chinese battery manufacturers to fulfil its ambitions.

ZF Friedrichshafen, the German vehicle technology provider, is another good example of the investment taking place across the industry. In recent years it has significantly expanded its development capabilities in autonomous driving and plans to invest €12bn in electromobility and autonomous driving over the next five years. In early 2019 it opened a new test centre for driveline technologies, creating additional testing capacities for electric, hybrid, and internal combustion engine drives.

Industry challenges

A recent report7 cited a number of key challenges facing the engineering sector:

- Polarisation of engineering skills - On the one hand, the increasing technical complexity of products requires more highly skilled systems engineers and architects. On the other, the increasing technical sophistication of products will require more scientific specialists.

Between the two the more simple and detailed design tasks are likely to be supported by IT tools and Artificial Intelligence (AI) systems - Work in open ecosystems - A growing and open ‘ecosystem’ brings several challenges. For example, car manufacturers must maintain control of all developments done by external suppliers and must be able to prove the robustness of their design in case of prosecution. Working efficiently with external players requires a common language and standard IT tools

- Product Data Management - Product Data Management (PDM) tools should promote company wide data sharing and can drastically accelerate new product development. But a gap exists between functionalities offered by IT engineering tools and the low adoption rate by engineers who are often reluctant to adopt new tools

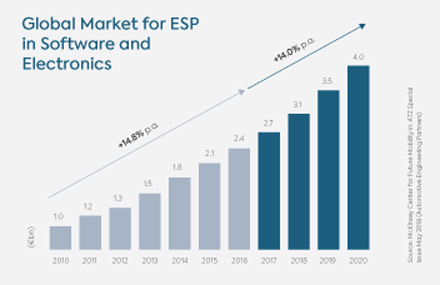

- Fully agile and digital development process - As the graph shows, the global market for ESP in software and electronics is forecast to grow from €2.7bn in 2017 to €4bn in 2020 at a CAGR of 14%. The growing importance of software for engineering new products has promoted agility in old fashioned engineering organisations. The next challenge is to convert hardware engineers to become more accustomed to digital development, and synchronise hardware and software development

- Use of product data to optimise design - With the cost of sensors and data processing rapidly decreasing, almost any object will be able to produce actionable data. Such data will provide valuable information to engineers on how their products are used in real life and the constraints they experience

- Customer-centric product design - B2B suppliers are increasingly focusing their innovation efforts on the needs of the final customer and are acquiring more and more user experience capabilities. New engineered products must not only match technical and functional specifications but also provide a unique ‘emotional’ experience

Leading players

Worldwide 15 top-selling ESP companies

Source: Automobilwoche

| Ranking | Company | Automotive sales 2017 (€m) | Total sales 2017 (€m) | Employees | Engineering focus |

|---|---|---|---|---|---|

| 1 | AVL List | 1,550 | 1,550 | 9,500 | Drive systems, testing technology, simulation |

| 2 | Bertrandt | 894 | 993 | 11,800 | Total vehicle, environmentally friendly mobility, autonomous driving |

| 3 | IAV | 798 | 798 | 7,000 | Powertrain, electronics and vehicle development |

| 4 | Edag Engineering | 717 | 717 | 8,404 | Total vehicle, production equipment, lightweight construction, e-mobility/car IT |

| 5 | Akka Group | 559 | 1,334 | 4,734 | Total vehicle, digitisation, autonomous driving, e-mobility |

| 6 | Horiba Automotive | 543 | 1,448 | 3,002 | Test systems, emissions measurement, vehicle tests, cyber security |

| 7 | FEV | 529 | 529 | 4,743 | Engines, alternative drives, E/E measuring and testing technology |

| 8 | Bosch Engineering | 520 | 570 | 2,100 | Software and function development, networking, E/E systems, IoT |

| 9 | Altran | 500 | 2,282 | 7,800 | Total vehicle, driver assistance, connected car, powertrain |

| 10 | Alten Group | 491 | 1,975 | 6,000 | E/E systems, car2X, interior, drive, validation |

| 11 | Magna Steyr Engineering | 380 | 380 | 2,100 | Total vehicle, engineering services, E/E, alternative drivetrain |

| 12 | Assystem Group | 274 | 700 | 4,200 | E-mobility, connectivity, driver assistance, safety/security, lighting |

| 13 | ETAS | 235 | 235 | 1,100 | Embedded systems, engineering, consulting/training |

| 14 | Applus IDIADA | 198 | 198 | 2,335 | Total vehicle, module and component development |

| 15 | Continental Engineering | 175 | 185 | 1,500 | Chassis, drive and interior electronics systems, prototype construction |

1: McKinsey & Co: Development Excellence – 'Capturing the full value of collaboration with engineering service providers'

2: Bertrand/Clearwater International

3: Berylis Strategy Advisers, ESP market update 2018

4: ResearchAndMarkets.com: Global Automotive ESP Market 2018-2022

5: Oliver Wyman analysis: EU Industrial R&D Investment Scorecard

6: eeNews: November 2018

7: Oliver Wyman Engineering 2030