InsurTech Clearview

Download PDF

Perspectives on the market

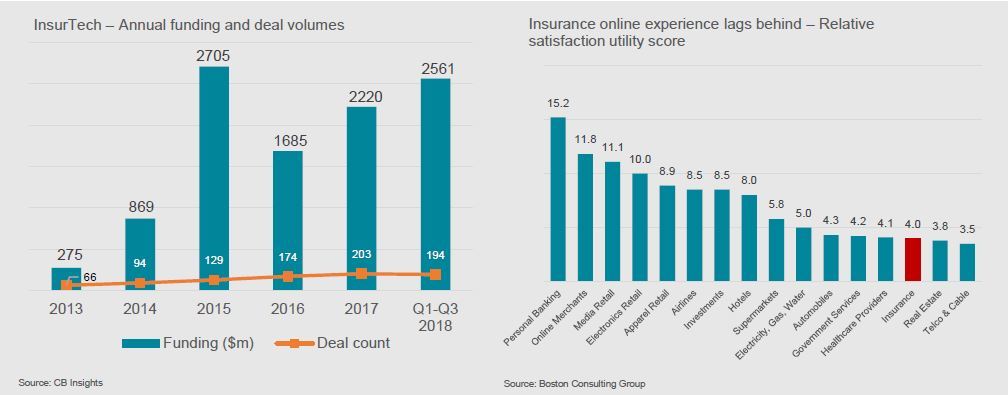

Unlike the FinTech industry where funding and follow-on investment growth have already started to decelerate in certain regions and segments of the market, the less mature InsurTech sector shows no sign of abating. Data from WTS reveals that global InsurTech investment totalled US$2.2bn (c. €1.9bn) in 2017, with both the volume and value of deals having more than doubled since 2014.

While banking and capital markets built up a considerable weight advantage by starting their FinTech journeys earlier, it is the insurance industry that will ultimately see the greatest benefit – and the highest levels of disruption – from this global upsurge of innovation.

The majority of large retail and investment banks embraced the FinTech concept several years ago. Their innovation and digital strategies are now relatively mature, whereas the picture within insurance is mixed. Insurance companies have not yet experienced the great disruption of the banking world, essentially for two reasons. Firstly they are inherently conservative, and secondly they operate in a highly regulated industry.

There are limits to how far big, traditional insurers can go when it comes to making the most of new developments, and outdated and unwieldy legacy technology platforms hinder insurers’ ability to create new products quickly.

As such, many disruptive operators have entered the market and upended traditional insurance across four main segments.

Distribution

Complex regulation, customer stickiness, and incumbents’ extensive underwriting skills built on years of experience and proprietary data have pushed disruptive newcomers to focus on the more easily accessible segments of the industry.

In particular they have concentrated on distribution and the more commoditised property and casualty (P&C) market which has become the most disrupted space over the past 10 years. Innovation has focused on digitalisation and mobile solutions, and improving direct-to-customer acquisition strategies through enhanced lead generation.

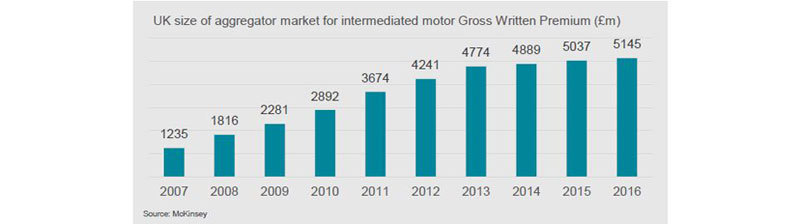

Today, UK insurance and financial services price and product comparison websites receive more than 26 million visits each month. Approximately 70% of car insurance policy switches and more than 65% of home insurance switches were derived from price and product comparison websites.

Deal activity

As the digital insurance distribution market becomes more mature, operators have gained significant scale and profitability levels and have been subject to increasing interest from financial and strategic acquirers.

In 2013 AnaCap backed the MBO of Simply Business, the UK’s leading digital SME insurance distribution platform, and generated a 4.5x return on its investment in the €140m sale to Aquiline Capital Partners. One year later, Aquiline sold the company to Travelers for approximately €465m, implying a multiple of 50x EBITDA. In November 2017, CPPIB invested €785m for a 30% stake in BGL Group, an online distributor of insurance products and operator of price comparison sites, for a multiple well over 10x EBITDA.

Omni-channel

To compete with newcomers, traditional insurers are moving steadily towards a digitally-enabled omni-channel distribution model. Every stage of the sales process is affected, from discovery of information through to advice and purchase.

Today 32% of P&C quotes are provided through digital channels, while the figure for life insurance is 27%. Both are expected to increase by approximately 10% in the next three years.

Underwriting & pricing

Insurers are increasingly automating processes such as policy underwriting and pricing. By harnessing the power of big data collected via the Internet of Things (IoT), Artificial Intelligence (AI), social media, and wearable/connected devices, insurers can provide more customised policies catering to the specific needs of policyholders, along with dynamic pricing. Furthermore, it enables insurers to provide real-time usage, such as mileage-based car insurance.

One example already in use is the way that Aviva prices its car insurance. Traditionally, this involved a lot of questions about the type of car, the location and the driving history. But the company has found a statistical link between the purchase of life insurance policies and safer driving, so life insurance policyholders get lower quotes.

Risk prevention

Technology is not only helpful in risk assessment, but also in prevention. Underwriters are using technology to process a vast amount of unstructured data while continuously learning from human interaction with data. For instance, insurers could alert customers of upcoming risks beforehand on their wearable and smart phone devices. This would also greatly benefit insurers as it would improve stickiness with policyholders and enable them to interact with customers more frequently. Health is one area where the potential for monitoring technology is moving ahead fast. South African insurer Discovery, creator of the Vitality programme, uses devices such as Fitbits or other activity trackers to encourage its health insurance customers to exercise more. The more they exercise, the fitter they are and so the cheaper the insurance.

Business process enhancement

Insurers are increasingly using automation and AI to supplement or even replace human decision-making.

Automation represents a significant opportunity for incumbents to cut costs as they face pressure to generate higher returns in the context of a low interest rate environment and limited organic growth due to subdued pricing.

Digital technology can help insurers simplify their operations, products and processes while improving efficiencies through reduced error rates.

Insurers hope that, in the short term, AI can help to automate some of the administrative processes that are done manually, and expensively, at the moment. For example, the ability to pre-populate application forms with customers’ data would help to cut hours from the application process.

Claims management

The other area where innovation can significantly improve insurers’ operations is claims management which has always been the weak point for insurers as the process often damages the relationship between carriers and their customers. Industry executives estimate that a customer who experiences a personal automotive claim could be up to 40% less likely to renew their policy, regardless of the outcome.

Innovation could help claims management become a powerful driver of customer satisfaction and retention. For instance, technology can be used to reduce or even eliminate inefficiencies embedded in legacy systems and processes. With digitalised real-time service models customers are given more control of the process by using automated loss notification, real-time processing, and predictive damage estimates based on photos of damages uploaded by customers, self-service capabilities and electronic payments.

Disruption

Newcomers are also focusing on digital disruption, such as sensors for monitoring homes and businesses, to mitigate risks and reduce the frequency and severity of claims, through to new data sources focused on loss prevention and incident management.

Recent technological developments could potentially shift insurers away from simply processing claims to actively mitigating risks – and therefore making losses smaller.

A notable transaction in the UK claims management market was the acquisition of Davies Group by HGGC for €105m. Davies Group is an insurance claims service provider, delivering third-party administration and specialist technical services to insurance intermediaries, the Lloyd's market, UK and global insurers, and large self-insured businesses.

Data analytics

Most insurers recognise the benefits of big data analytics and test-and-learn methods, which have great potential for understanding customer preferences, improving segmentation, and assessing customer risk by extracting insights to enable data-driven decision-making.

Newcomers in this space are focusing on data mining and modelling to quantify emerging risks including cyber security, new sources of data from sensors and communications technology to inform underwriting and pricing decisions, and automated machine learning supplementing human decision-making.