Dental

Market drivers

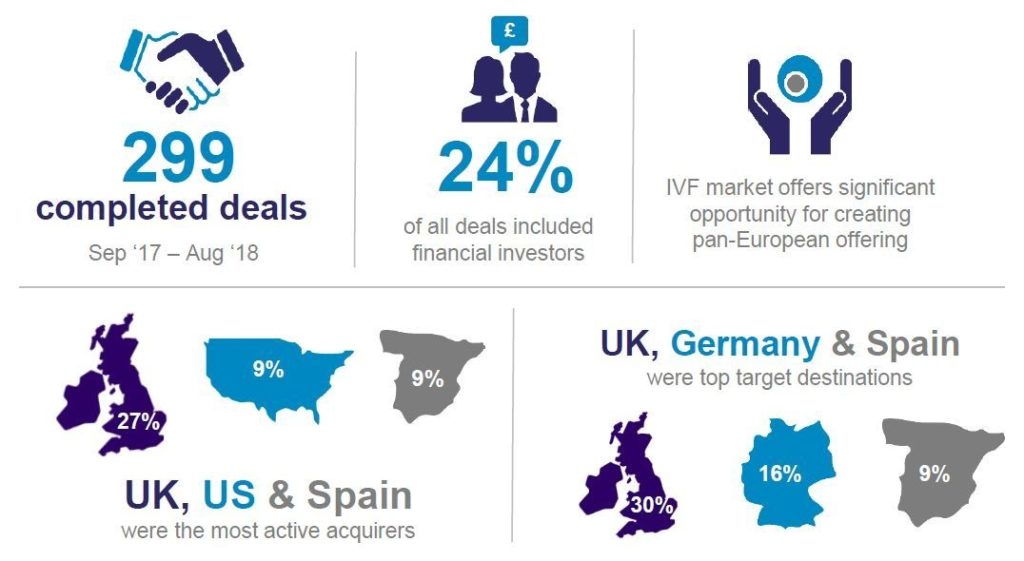

The sector across Europe remains highly fragmented and presents a significant investment opportunity for financial investor firms and strategic buyers from adjacent healthcare sectors.

In the UK a new NHS contract is due to be in place by the end of 2019. This is expected to provide more predictable incomes for practices through a greater emphasis on remuneration through capitation.

High barriers to entry provide opportunities for continued consolidation and growth for established players.

In Germany, the market is highly fragmented. A regulatory change in 2015 allowed outpatient service providers to offer single specialisms, making it easier for dental practices to amalgamate into groups.

Investment thesis

Further consolidation of the market is likely in most western European countries. The market is being specifically targeted by financial investor firms and is attractive to possible pan-European players.

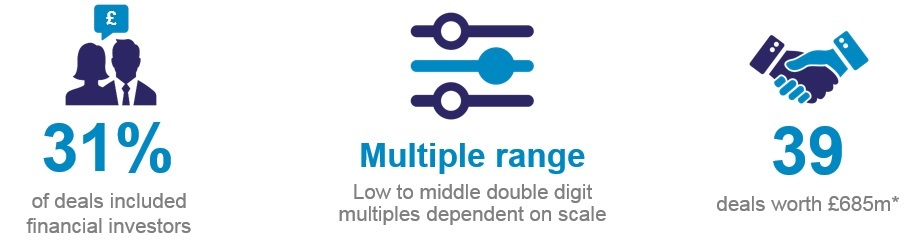

Trade activity

- Colosseum Dental Group (Norway) acquired Oral Hammaslääkärit (Finland) - Oral is the leading Finnish private dentistry chain with 63 clinics. The deal gives the enlarged Colosseum Group sales of around £266m from 200 clinics across Scandinavia, the UK, Switzerland and Italy as it seeks to build a leading pan-European dentistry group.

EV: n.a, EBITDA: n.a - Portman Healthcare Limited (UK) acquired Watson Dental Ltd (UK) - Portman Healthcare is one of the leading dental care providers in the UK and has been growing rapidly by organic and acquisition growth since it was acquired by private equity firm Livingbridge, which recently sold the business to Core Equity (see right).

EV: n.a, EBITDA: n.a

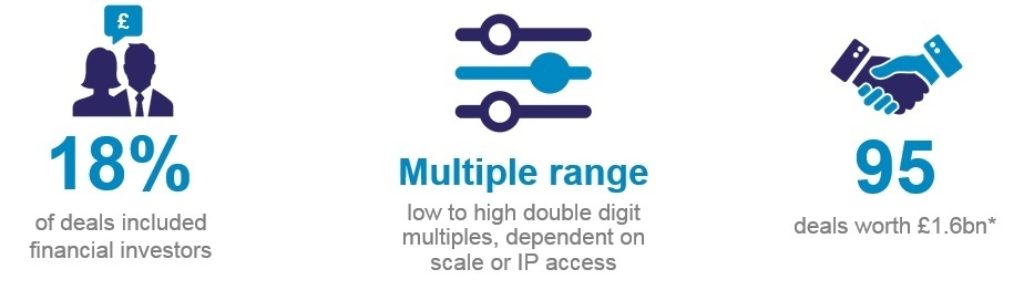

Financial investor activity

- Nordic Capital (Sweden) acquired three dental clinic companies from Hesira (Switzerland/Netherlands) - Nordic Capital acquired Dental Clinics Nederland and TopOrtho, consisting of 88 clinics in the Netherlands, and Adent Cliniques Dentaires Groupe, a 22-site operator in Switzerland, from Oaktree Capital. Nordic also bought Germany’s largest dental laboratory owner, DPH Dental Partner Holding, and SFE Beteiligungsgesellschaft, owner of six clinics in Cologne that operate under the Zahnstation brand. Nordic Capital is creating a leading pan-European dental group and will pursue further acquisitions.

EV: c.£372.7m, EBITDA: c.16x - EQT Partners AB (Sweden) acquired Curaeos B.V. (Netherlands) - Curaeos is a major dental care provider based in the Netherlands. Its patient base covers over 1 million customers through its pan-European network of more than 220 clinics.

EV: n.a., EBITDA: c.20x - CBPE Capital (UK) acquired Rodericks Dental (UK) - Rodericks is a leading provider of NHS, private and specialist dental services and owns 71 practices in England and Wales. CBPE has invested in the business as part of plans to increase the number of practices and broaden the range of dental services offered.

EV: n.a, EBITDA: n.a - Core Equity (Belgium) acquired Portman Dental (UK) - Belgium-based private equity firm Core Equity has bought UK based dental chains operator Portman Dental. Portman has grown rapidly under the previous ownership of Livingbridge and it now operates over 80 dental chains across the UK, a sharp rise from the 27 practices it operated in 2014.

EV: c.£300m, EBITDA: n.a

Sponsor backed platforms to note:

- Sponsor: CBPE

Company: Rodericks Dental

Country: UK

Revenue: £51m

EBITDA: £5m

Invested: Sept 2017 - Sponsor: Nordic Capital

Company: Three dental clinics of Hesira Group

Country: Netherlands

Revenue:£116.5m

EBITDA: £21.5m

Invested: Feb 2018 - Sponsor: Jacobs Holding

Company: Colosseum Dental Group

Country: Norway

Revenue: £102.4m

EBITDA: £8.7m

Invested: Jan 2017 - Sponsor: EQT

Company: Curaeos B.V.

Country: Netherlands

Revenue: £75.3m

EBITDA: n.a.

Investment: Oct 2017