European overview

Download PDF

This report identifies key themes driving European Private Equity (PE) deals’ EV/EBITDA multiples on a quarterly basis. The objective is to assist PE investors in understanding drivers behind value trends across regions and sectors, leading to good investment opportunities.

The deals market was substantially impacted in Q2 2020 as deals in their infancy stages were put on hold to wait out the unfolding situation across the globe however, Q3 2020 marked a rebound in activity with record levels of deal completions. High-quality businesses in resilient sectors such as healthcare/pharma services and TMT were highly sought after by the European PE market as the globe emerged from lockdown and PE looked to deploy capital, increasing valuations in these thriving sectors.

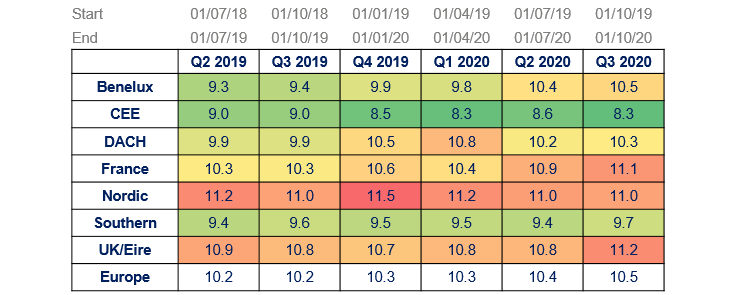

In Q3 2020, average multiples paid in PE-backed transactions throughout Europe increased slightly when compared with the previous quarter and the same quarter in 2019, with deal volume increasing 58% compared to the previous quarter.

The UK and Ireland was the hottest region for multiples in the quarter, also seeing the largest increase in valuations of any region, up 4% against Q2 2020 and against the same quarter in 2019, bringing average valuations in the region above 11x. The UK also experienced a substantial increase deal volume of 80%, although volume remains lower than the same period in 2019 and average pre-COVID activity levels.

France saw one of the largest increases in valuations during the quarter, up 2% against Q2 2020 and up 8% in comparison to the same quarter in 2019 bringing the valuations above 11x. France also experienced a 70% increase in deal volume in comparison to Q2 2020 brining the volume average close to pre-COVID activity levels.

The third hottest region in Europe for the quarter was the Nordic region, despite no change in valuations, deal volume increased by 83% in comparison to the previous quarter and a 74% increase in comparison to the same period in 2019. For the fifth quarter in a row, the Nordic region has seen multiples of over 11x. A similar valuation trend was experienced in the Southern region however, average valuations were sub 10x for the sixth quarter in a row. Deal volumes in the region increased by 213% in comparison to the previous quarter and reached higher levels than pre-COVID activity levels.

The DACH region experienced an increase in valuations and deal volume, with a 1% increase in average valuations in Q3 2020 representing a 4% increase in comparison to the same quarter in 2019. The region also experienced the greatest volume of transactions in the quarter, a trend also seen in Q2 2020.

The TMT sector experienced the largest number of PE-backed transactions for the third quarter in a row

The TMT sector experienced the largest number of PE-backed transactions for the third quarter in a row as the resilience of the sector continues to attract interest from PE looking to deploy capital. Despite a 2% decrease in valuations compared to the preceding quarter, valuations have remained in line with the same period in 2019.

The hottest sector for the quarter in terms of valuations was financial services, with valuations increasing 8% in comparison to the previous quarter and 15% when compared to Q3 2019. Deal volume in the sector also increased by 40% although down on the same period in 2019.

valuations in healthcare for Q3 2020 exceeded 11x for the first time in more six quarters

The second hottest sector for the quarter in terms of valuation was healthcare, with valuations for Q3 2020 exceeding 11x for the first time in more six quarters demonstrating the value of healthcare assets in the current climate. The volume of deals increased 14% on the previous quarter, a trend expected continue into the final quarter of 2020.The food and beverage sector experienced a substantial increase in deal volumes, bringing activity levels in line with pre-COVID levels. The sector also experienced an 8% increase in valuations compared to the previous quarter, increasing valuations over 10x for the first time in over six quarters, a 10% increase on the same period in 2019.

The food and beverage sector experienced a substantial increase in deal volumes, bringing activity levels in line with pre-COVID levels. The sector also experienced an 8% increase in valuations compared to the previous quarter, increasing valuations over 10x for the first time in over six quarters, a 10% increase on the same period in 2019.

Industrials and chemicals and business services both experienced increases in deal volumes in the quarter, 111% and 40% respectively. However, valuations decreased 3% in industrials and chemicals whilst business services experienced a 6% increase. This was the fourth quarter in a row that business services endured an increase in average multiples paid in PE-backed transactions.

In terms of deal size, and in line with most quarters historically, the largest volume of deals was in the sub €50m category. Conversely, the smallest volume of deals was experienced in the >€1bn range.For the fifth quarter in a row, the richest valuations were seen in transactions >€1bn, increasing 8% on the previous quarter. The second hottest valuations were seen in the €250m-€500m range which saw an increase of 15% on the previous quarter and 30% on the same period in 2019.

Deals in the €500m-€1bn range continued to show increasing valuations however only up 1% when compared to the previous quarter and down 6% in comparison to the same quarter in 2019.

In this quarter, the Multiples Heatmap focuses on trends seen in Sweden where a lockdown has not yet been enforced by the Government and the TMT sector where deal activity levels remain high.

Averages over the last twelve months